If your company is still working through its IFRS 16 transition or you’re reviewing past decisions one question comes up more than almost any other:

Which transition method should we use?

The short answer is: it depends on your leases, your reporting goals, and how much effort your team can absorb. But once you understand what each method actually does to your numbers, the choice becomes a lot clearer.

Let’s break it down in plain language.

A Quick Recap: What Is IFRS 16 Asking You to Do?

Under IFRS 16, almost every lease you hold, property, equipment, vehicles, must now appear on your balance sheet as a right-of-use (ROU) asset and a corresponding lease liability. This replaced the old IAS 17 model, where most operating leases simply stayed off-balance-sheet entirely.

The big practical challenge during transition is this: you have a portfolio of existing leases that were accounted for under the old rules. How do you bring those onto the balance sheet under the new rules — without rewriting your entire financial history?

That’s exactly what the two transition methods address.

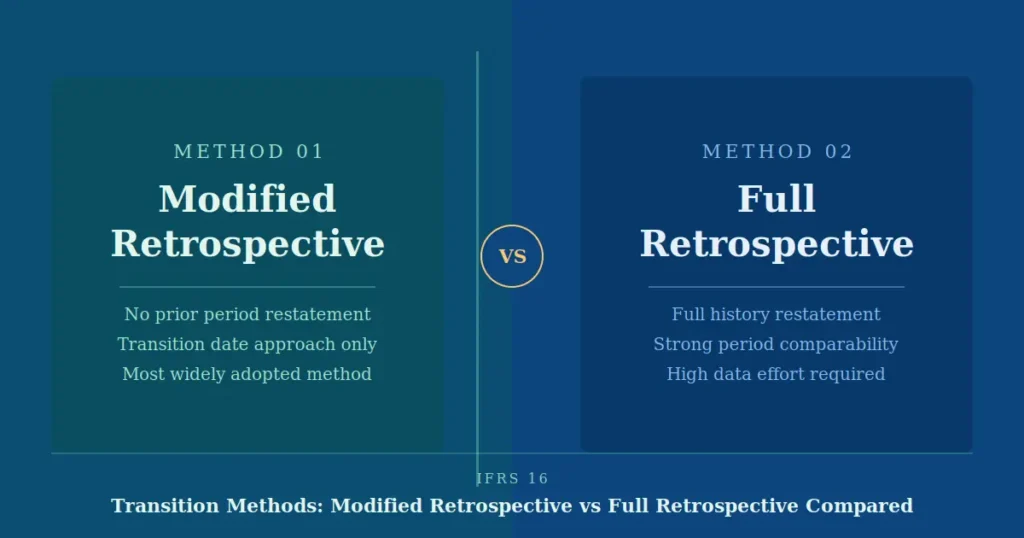

Method 1: Full Retrospective Approach

The full retrospective method asks you to go back in time all the way to when each lease started and restate your financials as if IFRS 16 had always been in place.

What this means in practice:

-

- You recalculate the lease liability and ROU asset from the lease commencement date

-

- Comparative prior-period figures are restated

-

- The cumulative impact is recognised in retained earnings at the start of the earliest comparative period presented

The upside:

Comparability. Your current and prior-year financials follow the same accounting basis, which makes trend analysis meaningful and is generally preferred by analysts and investors who want a clean like-for-like view.

The downside:

It is significantly more work. You need historical data going back to the inception of every in-scope lease — discount rates that applied at the time, original lease terms, modification history. For companies with large, complex lease portfolios, this can be an enormous data-gathering exercise.

Method 2: Modified Retrospective Approach

The modified retrospective method takes a more pragmatic route. Instead of restating history, you recognize the cumulative effect of IFRS 16 as a single adjustment to opening retained earnings on the date of initial application (typically 1 January 2019 for most calendar-year reporters).

Prior periods are not restated. Your comparative figures stay as they were under IAS 17.

What This Means In Practice:

-

- You measure the lease liability at the present value of remaining lease payments, discounted using the incremental borrowing rate at the transition date

-

- The ROU asset can be measured in one of two ways: either equal to the lease liability (adjusted for any prepaid or accrued lease payments), or as if the standard had always applied but using the transition date discount rate

-

- The practical expedients available under this method are broader and more flexible

The Upside:

This is the method most companies chose — and for good reason. It requires less historical data, it is faster to implement, and the practical expedients (like exempting short-term leases and low-value assets) reduce the volume of work considerably.

The Downside:

Your year-one comparatives won’t be on the same basis as your post-transition figures. Stakeholders reviewing multi-year trends will see a visible “step change” in balance sheet size and EBITDA presentation at the transition date.

Side-by-Side Comparison

| Factor | Full Retrospective | Modified Retrospective |

|---|---|---|

| Prior period restatement | Yes | No |

| Data requirement | High — inception-to-date | Lower — transition date only |

| Implementation effort | High | Moderate |

| Comparability | Strong | Limited at transition point |

| Practical expedients | Limited | Extensive |

| Most common choice? | Less common | Widely adopted |

Which Method Is Right for Your Business?

Here is a simple way to think about it:

Choose full retrospective if you are a listed company under close analyst scrutiny, you have a manageable lease portfolio with good historical records, or your stakeholders explicitly want clean comparable financials.

Choose modified retrospective if your lease data from prior years is incomplete or difficult to reconstruct, you are under time pressure to transition, or you have a high volume of leases where the practical expedients will significantly reduce the workload.

For most mid-sized businesses, the modified retrospective method is the practical winner. It gets you compliant without the cost and complexity of a full historical restatement.

One Thing That Affects Both Methods: The Discount Rate

Regardless of which approach you take, the discount rate you apply has a major effect on your lease liability figures. Even a 1% difference in the incremental borrowing rate can shift your total recognized liability by tens of thousands, or in large portfolios, millions of pounds or dollars.

This is exactly where an IFRS 16 transition impact calculator pays for itself. Instead of manually running sensitivity scenarios in spreadsheets, a purpose-built tool lets you model different rate assumptions, lease terms, and exemption options, and see the balance sheet impact in minutes.

Final Thought

Neither method is universally “better.” The best choice depends on your data, your stakeholders, and your capacity. What matters most is that the decision is made deliberately, with a clear understanding of what each method does to your reported numbers and how it will be perceived by auditors, investors, and lenders.

If you have not yet modelled the full financial impact of your lease portfolio under both approaches, now is the right time to do it.